Build a Wire-Instruction Verification Desk Before AI Sends Closing Updates

Build a Wire-Instruction Verification Desk Before AI Sends Closing Updates

AI can make closing communication feel organized. It can summarize title emails, draft buyer reminders, turn a settlement checklist into a friendly note, and keep the CRM timeline current while the transaction coordinator is buried in deadlines. That speed is useful, but it creates a specific risk: the system may treat a payment instruction, a changed bank account, or a rushed deadline as just another message to route.

That is the wrong abstraction. Wire instructions are not normal transaction content. They are a high-risk control point that should sit outside ordinary follow-up automation.

The FBI Internet Crime Complaint Center reported more than one million complaints and $20.877 billion in reported losses in 2025. Business email compromise alone accounted for more than $3.0 billion in reported losses, while real estate was listed with $275.1 million in reported losses. The same report also tracks an AI-related descriptor, which is a reminder that fraud and automation are now evolving together. For real estate teams, this means the closing workflow needs a verification desk before AI is allowed to summarize, send, escalate, or rewrite anything connected to wiring money.

The point is not to make AI avoid closings. The point is to make the system know which parts of the closing are clerical and which parts require a human control.

Why this belongs in operations, not just training

Most wire-fraud advice tells buyers to call a trusted party, confirm instructions by phone, and avoid relying on email alone. That advice is right, but it is usually aimed at the consumer. A brokerage or team needs an internal operating layer that makes the safe behavior the default.

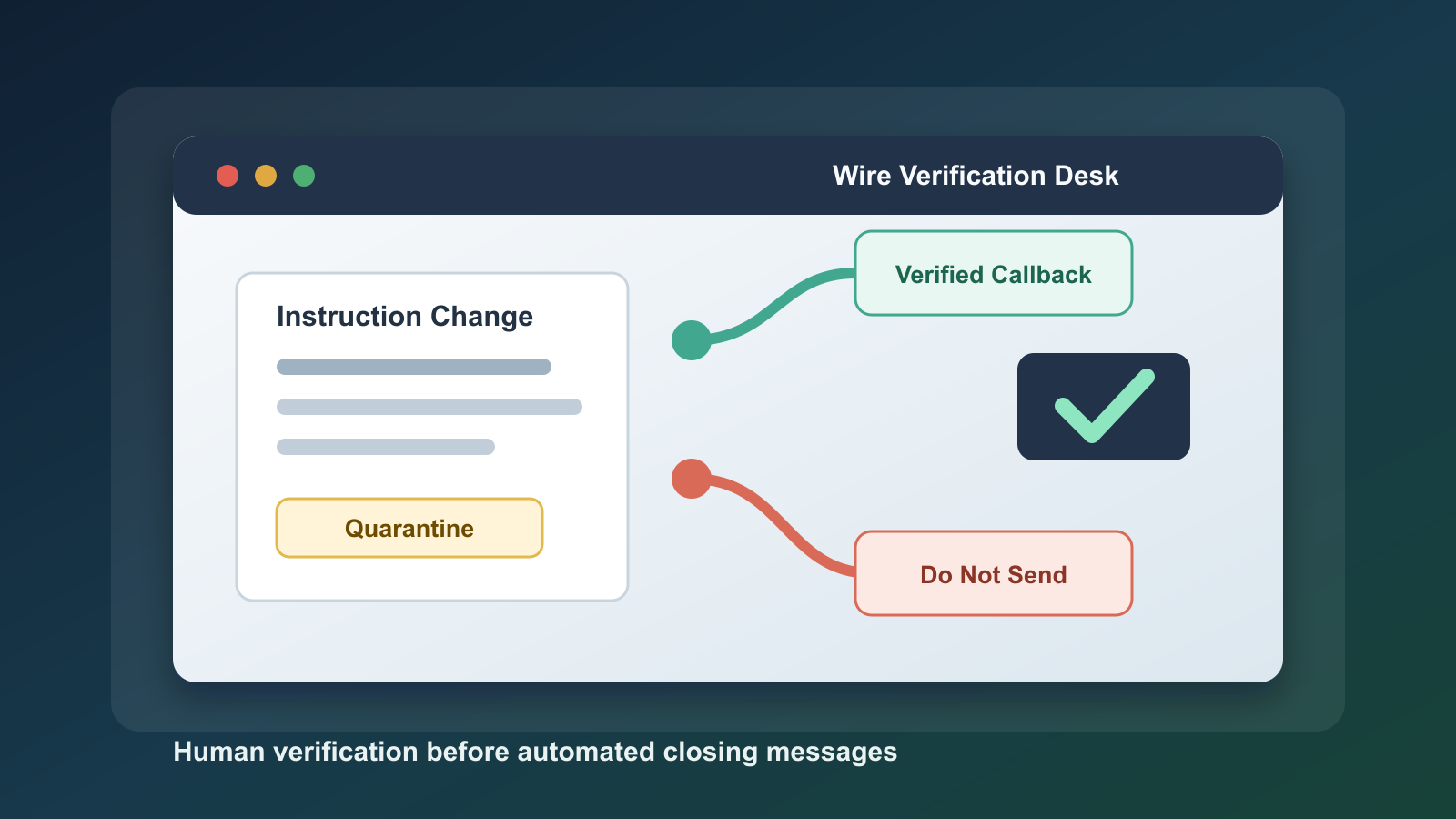

That layer is a wire-instruction verification desk. It is a small workflow surface inside the CRM or transaction system that records who is allowed to provide instructions, where those instructions came from, who verified them, what callback number was used, whether any change request appeared, and which messages AI is allowed to send.

Without that desk, automation can accidentally make weak process look polished. A spoofed email can be summarized cleanly. A changed instruction can be copied into a client update. A vague closing reminder can be made more persuasive. The writing gets better while the verification stays missing.

NAR's 2025 Technology Survey shows how quickly real estate professionals are adopting digital tools: eSignature remains deeply embedded, social media is near universal, and many agents are already using AI-generated content. That adoption is not the problem. The problem is allowing a content tool to touch a payment-control workflow without a separate evidence gate.

What the desk should contain

The desk should be boring by design. If it feels like a clever AI feature, it is probably too loose.

Start with an approved-party register. For each active transaction, the team should store the title or escrow contact, lender contact, attorney contact where applicable, internal transaction owner, and the approved callback numbers gathered from a known source. The callback number should not be copied from the same email that contains the instruction change. It should come from the engagement letter, secure portal, prior verified record, or direct known contact.

Next, add an instruction-source log. Every payment-related instruction should be tagged by source: secure portal, in-person document, verified phone call, lender document, title-company package, or unverified email. AI can read the log, but it should not be allowed to upgrade the trust level. Only a human reviewer should move an item from unverified to verified.

Then create a change-request quarantine. Any message that mentions a new wire account, changed routing number, urgent payment deadline, inability to accept a check, alternate recipient, or last-minute closing-fund adjustment should be routed into a blocked state. In that state, AI may draft an internal summary for the transaction owner, but it may not send client-facing instructions, update the CRM payment fields, or mark the closing task complete.

Add a confirmation record. The confirmation should capture who called, who answered, which known number was used, what was confirmed, when it happened, and whether the client received the team's standard warning. Keep this concise. The goal is not a legal memo. The goal is a repeatable control that a manager can audit in thirty seconds.

Finally, define the approved client language. AI can help write reminders, but payment language should be constrained to a promise library. Good default language says the team will not send changed wire instructions by ordinary email, clients should verify instructions through trusted contacts, and urgent change requests should be treated as suspicious until confirmed. The model should select from approved language, not invent new reassurances.

How AI should interact with the desk

The safest pattern is a permission model, not a prompt.

If the transaction has no verified instruction record, AI can prepare a task for the transaction owner: verify payment process before sending closing reminder. It can summarize the missing fields. It can suggest which known contacts need confirmation. It should not tell the client where or how to send funds.

If an instruction exists but has not been confirmed, AI can write an internal checklist. It should flag the communication as high risk, include the source, and ask for a verified callback. It should not convert the information into client-facing payment guidance.

If a change request appears, AI should stop the normal workflow. That means no automatic reply, no friendly rewrite, no CRM update, and no task marked complete. The only allowed action is escalation to the transaction owner with the suspicious indicators highlighted.

If the instruction is verified, AI can help with low-risk communication: remind the client to review closing documents, confirm the date and location, tell them who to contact with questions, and repeat the team's standard anti-fraud warning. Even then, the model should not paste sensitive banking details into ordinary messages.

This is how automation becomes useful without becoming authoritative over money movement.

The fields to add to the CRM

A practical desk can start with a handful of fields:

- Closing payment status: not needed, pending verification, verified, changed, blocked.

- Payment-instruction source: secure portal, verified document, verified call, email only, unknown.

- Trusted callback source: engagement record, prior verified CRM contact, secure portal, other.

- Verification owner: the human responsible for the control.

- Verification timestamp: when the call or secure confirmation happened.

- Change-request detected: yes or no.

- AI send permission: internal summary only, approved warning only, normal closing update allowed.

- Incident path: title company, lender, broker, bank, IC3, client.

These fields matter because they give the automation something concrete to respect. A generic instruction like 'be careful with wire fraud' is not enough. The CRM needs structured state that blocks unsafe actions.

The operating cadence

Use the desk at four moments.

First, when a transaction opens, add the approved-party register before any closing-related automation starts. Second, when closing instructions are expected, require the source log and confirmation record. Third, when any instruction changes, quarantine the workflow and require a manager review. Fourth, after closing, archive the verification record with the transaction file so the team can audit what happened.

For teams that already use AI summaries, the immediate improvement is simple: add a rule that any payment-related text goes to internal review, not client output. Then add the CRM fields. Then add reporting: blocked change requests, missing verification records, and messages where AI was limited to internal summary only.

The test

A wire-instruction desk is working when three things are true.

A transaction coordinator can look at the CRM and know whether payment communication is allowed. A model can detect risky language but cannot send or store payment instructions without verified state. A manager can audit the last ten closings and see the source, owner, timestamp, and escalation outcome for each payment-control moment.

That is the standard. Not more content. Not faster replies. Verified state before automated closing communication.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile