Build a Lender SLA Board Before AI Recommends Financing Partners

Build a Lender SLA Board Before AI Recommends Financing Partners

The next weak spot in AI-assisted real estate operations is not another lead form or a faster chatbot. It is the moment an AI system starts recommending financing partners, drafting loan-status updates, or ranking buyer readiness from stale lender notes. A buyer can look strong in the CRM and still be exposed if the lender has not confirmed the current rate lock, missing conditions, appraisal timing, insurance assumptions, or whether the buyer's documentation still supports the offer strategy.

That is why real estate teams need a lender SLA board before they let AI route buyers to financing partners or summarize mortgage status for clients. The board is not a public leaderboard and it is not a promise that one lender is always better than another. It is a working control surface that shows which financing partners have current service evidence, what type of buyer situation they handle well, how quickly they respond, and where a human has to review before an AI recommendation goes out.

The market makes this practical rather than theoretical. NAR's current REALTORS Confidence Index shows contracts still typically close in 30 days, while 13% of contracts had delayed settlements and 5% were terminated in the latest reporting window. MBA's April 30, 2026 Purchase Applications Payment Index shows affordability pressure moving again, with the national median payment applied for by purchase applicants rising from February to March. ICE's March 2026 Mortgage Monitor shows how quickly rate shifts can reshape borrower opportunity and lender volume. In that environment, the lender note that was acceptable last month can be wrong enough to create a bad client update today.

AI raises the stakes because it can make the wrong routing decision look polished. It can write a confident buyer update from a three-week-old preapproval email. It can recommend a lender because the partner converted three older files, while missing the current backlog or a pattern of late condition reviews. It can summarize a loan file without knowing that the buyer changed jobs, the HOA packet is delayed, the insurance quote changed the payment, or the lender's published response time no longer matches actual behavior.

A lender SLA board gives the AI a smaller, cleaner operating lane.

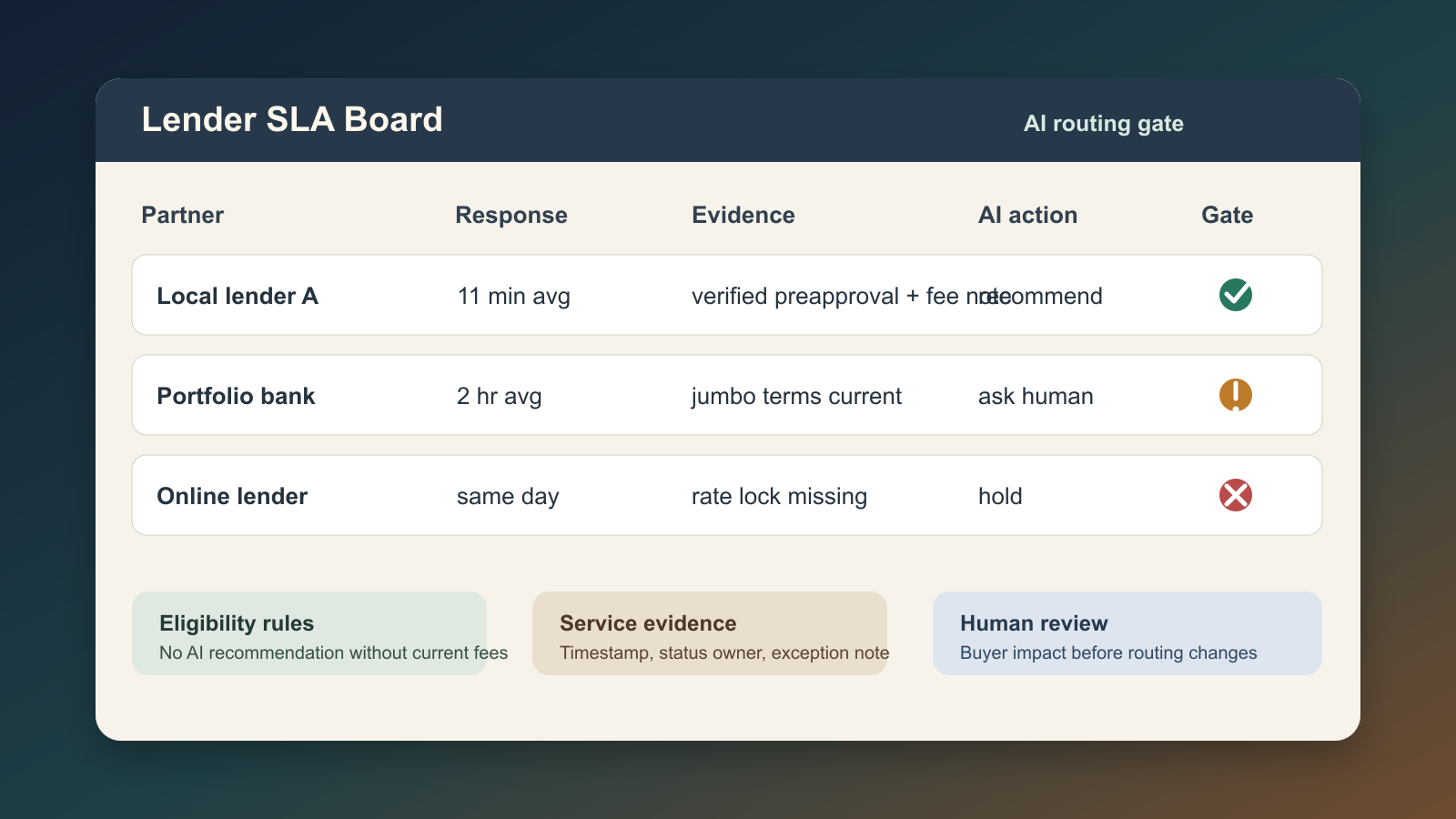

What belongs on the board

Start with a row for every lender, loan officer, mortgage broker, portfolio bank, credit union, and specialty financing partner that the team might mention to a buyer. Do not rank them by preference first. Rank them by evidence completeness.

The minimum fields are simple: partner name, licensing or coverage notes, loan types supported, markets served, latest confirmed response time, last verified fee or pricing note, document condition turnaround, appraisal coordination pattern, closing disclosure readiness, escalation owner, and the date each field was last verified. Add one field that matters more than most teams expect: AI eligibility.

AI eligibility should be one of four states.

Use eligible when the partner has current pricing context, current process notes, recent successful file evidence, and a named human escalation path. Use limited when the partner can be included in a shortlist but not recommended as the primary option without review. Use hold when pricing, response, capacity, or licensing evidence is stale. Use blocked when there is a known unresolved service issue, compliance concern, client complaint pattern, or missing human owner.

This turns lender selection from memory into operations. The AI no longer asks, who do we usually use? It asks, which partners are currently eligible for this buyer's scenario?

Track service levels by buyer impact

The useful SLA metrics are not vanity metrics. Average response time is helpful, but only when it is tied to transaction risk. A lender who answers fast but misses conditions is not operationally stronger than a lender who answers in two hours and catches the issue that would delay closing.

Track these service levels by business consequence:

- Time to first buyer response after referral

- Time to verified preapproval or updated qualification

- Time to disclose missing documents or loan conditions

- Time to confirm rate-lock status and expiration

- Time to respond to appraisal, insurance, HOA, title, or income changes

- Time to provide a closing-readiness update once under contract

- Number of files needing broker, team lead, or client-service escalation

Each metric needs a timestamp, source, and owner. A CRM task is not enough. The board should show whether the source was a lender email, call note, secure portal update, document request, buyer confirmation, or transaction coordinator review. If the AI cannot trace the evidence, it should not convert that evidence into advice.

Separate recommendation from explanation

A common implementation mistake is letting AI both choose the lender and explain why. Those are different permissions.

Recommendation means the AI can include a financing partner in a buyer workflow, shortlist, or internal routing suggestion. Explanation means the AI can tell a client why a partner may fit the situation. The second permission should require stronger evidence because it creates more client reliance.

For example, an AI assistant might be allowed to say, "I am routing this to our lending review queue because your offer timing is tight." It should not say, "This lender is the best option for you," unless the board has current evidence for pricing context, speed, file type, buyer needs, and human review. The FTC's mortgage shopping guidance still points consumers toward comparing terms, fees, APR, and total payment rather than trusting a single advertised rate or simple monthly-payment claim. AI should reinforce that discipline, not shortcut it.

Build the human review gate

The strongest insight from recent buyer research is that consumers are becoming comfortable with AI in the process while still wanting human verification. Cotality reported on April 16, 2026 that 75% of homebuyers expect AI in the homebuying process, and 44% would pay for a human expert to verify AI-generated housing decisions. NerdWallet's 2026 Home Buyer Report found that 48% of prospective buyers have used or will use AI tools during the homebuying process, including for cost estimates and guidance, but advised buyers to verify because AI can lack nuance.

That is the operating model for lender routing: AI can organize, compare, remind, and escalate, but a person signs off before a financing recommendation becomes client-facing advice.

The board should trigger review when any of these conditions are true:

- The buyer is near debt-to-income, cash-to-close, credit, or appraisal limits

- The lender evidence is older than the team's freshness threshold

- The buyer is using a specialty product, assistance program, bridge option, portfolio loan, or nonstandard income documentation

- The AI wants to change a recommended partner from the team's default pattern

- The lender has an unresolved service exception in the last 30 to 60 days

- The update would mention rate, affordability, approval confidence, closing certainty, or payment assumptions

This keeps the AI useful without making it the authority on a regulated financial decision.

Make the board operational in one week

Do not start with a perfect integration. Start with the files already moving through the business.

Day one: export the last 20 to 50 buyer transactions and identify every lender or mortgage partner that touched a file. Day two: create the board fields and mark every partner as hold until current evidence is verified. Day three: ask the team to log three timestamps per active financing file: referral sent, lender first response, and verified status update. Day four: add escalation reasons from recent delayed or stressful files. Day five: define the AI eligibility states and block client-facing recommendations when evidence is stale.

Only after that should the team connect the board to CRM automation. The first automation can be small: when a buyer moves to active offer preparation, the system checks whether the recommended financing partner is eligible, limited, hold, or blocked. If limited or hold, it opens a human review task. If eligible, it lets AI draft an internal routing note with evidence links. Client-facing copy still waits for review when the message includes affordability, loan confidence, rate-lock, or closing-certainty language.

The payoff

The point is not to make AI sound more confident about lenders. The point is to make the business more honest about what it knows.

A lender SLA board helps a brokerage protect buyers from stale assumptions, helps agents stop relying on memory, helps transaction coordinators spot weak handoffs earlier, and gives AI a verified operating surface. It also creates a fairer relationship with financing partners because performance is evaluated by current evidence, file fit, and service exceptions rather than whoever got the last referral.

Before AI recommends a lender, make it prove the partner is current, suitable, responsive, and reviewable. That is the difference between automation that helps the client and automation that simply says the risky thing faster.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile