Build a Referral Handoff Ledger Before AI Routes Clients

Build a Referral Handoff Ledger Before AI Routes Clients

AI can now read a CRM note, detect that a buyer needs a lender, inspector, title contact, insurance quote, moving help, or attorney, and draft a polished referral message in seconds. That sounds useful until the system quietly turns one messy operational question into three bigger problems: it recommends the wrong partner, it skips the client's choice, or it creates compensation and disclosure risk that no one reviewed.

Real estate teams should not treat partner routing as a copywriting task. It is an accountability task. The practical layer is a referral handoff ledger: a compact operating record that says which outside providers are eligible, why they are eligible, what relationship or compensation context exists, what the client was told, and who approved the handoff before AI sends anything.

This matters because AI is moving into the transaction while clients are still asking for human certainty. NAR's 2025 Technology Survey found broad technology adoption among Realtors, including AI-generated content use, while Cotality's April 2026 homebuyer research found that buyers expect AI in the process but still want human verification around consequential decisions. That combination creates a simple operating standard: automation can prepare the handoff, but a human-owned ledger should control whether the handoff is allowed.

The failure mode is invisible steering

A referral problem rarely looks dramatic inside the CRM. It starts with a note like "needs lender" or "send inspector options." An AI assistant sees the note, looks at past activity, chooses the partner most often used by the team, drafts a message, logs the task, and marks the workflow complete.

The problem is that frequency is not the same as suitability. The most common partner may be overloaded, outside the client's geography, missing a needed specialty, unavailable on the required timeline, or tied to a financial relationship that requires disclosure and review. If the model learns from old notes, it may also repeat stale preferences long after a partner's performance or availability changed.

The risk gets sharper around settlement services. CFPB's current Regulation X section on RESPA prohibits fees, kickbacks, or other things of value tied to settlement-service referrals for federally related mortgage loans, and it defines referral influence broadly. CFPB's RESPA FAQ also stresses that marketing services and referral activity require fact-specific analysis. That does not mean teams should freeze. It means AI should not be the first system deciding which client gets routed to which provider.

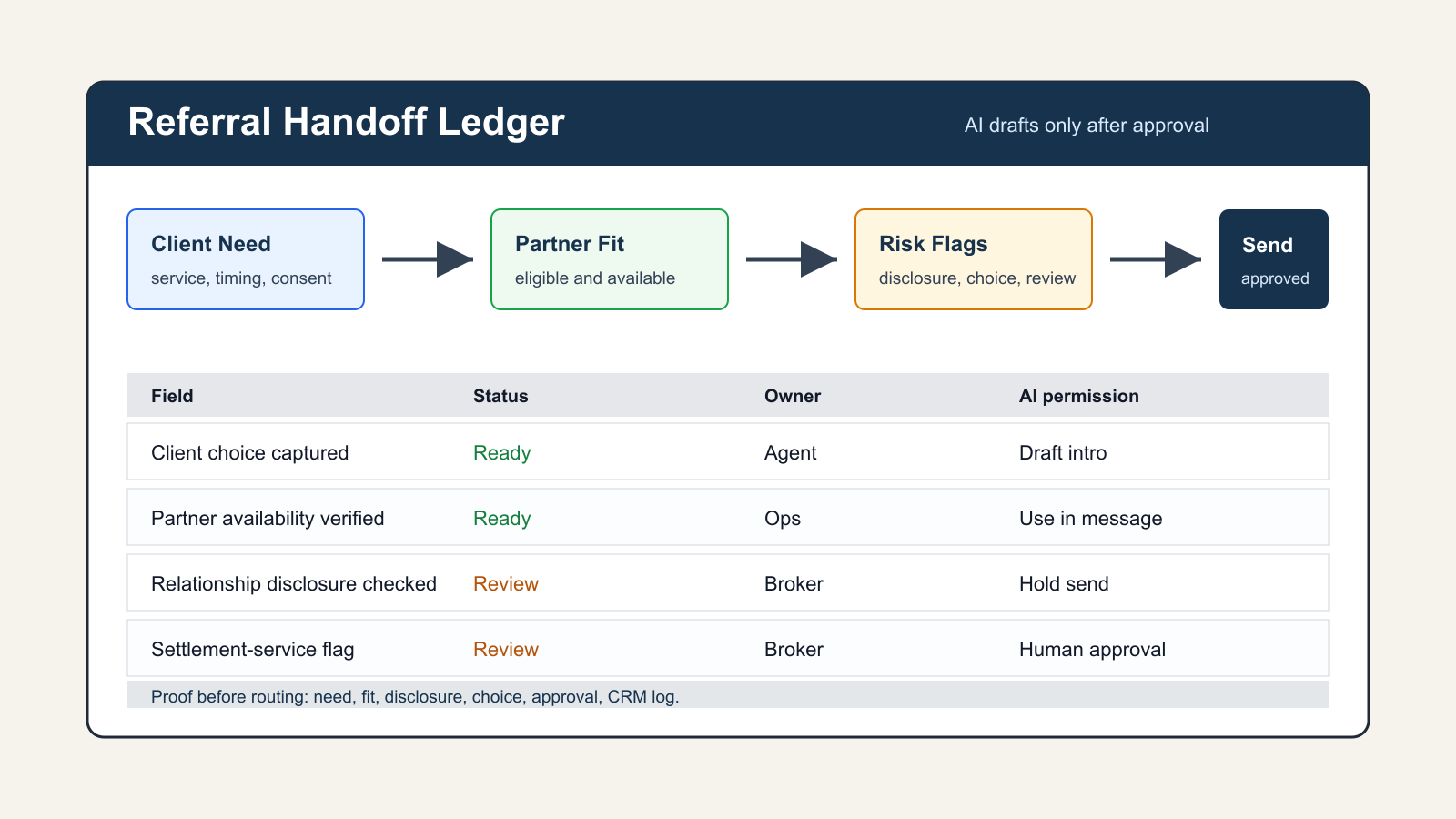

What the ledger has to prove

A referral handoff ledger does not need to be complicated. It needs to make the decision auditable before the message leaves the business.

Start with the client context. Record the service need, location, timing, budget sensitivity, language or accessibility needs, representation status, and any constraints already stated by the client. If the client asked for three options, the ledger should not allow AI to send one preferred option. If the client asked for a specialist, the ledger should not route to a generalist because that name appears most often in the CRM.

Next, record partner eligibility. Each partner row should show service category, coverage area, current availability, license or qualification fields when relevant, last verified date, owner, response-time history, and disqualifying conditions. An inspector who is excellent but unavailable this week should not be treated as eligible for an inspection period that expires Friday. A lender who performs well for conventional buyers may not be the right default for a self-employed buyer without a current suitability note.

Then add relationship and compensation context. The ledger should separate cooperative brokerage referrals, ordinary vendor lists, marketing arrangements, affiliated business relationships, and settlement-service providers. It should flag anything that needs disclosure, counsel review, brokerage approval, or a client-choice step. The purpose is not to turn every agent into a lawyer. The purpose is to keep AI from hiding a compliance-sensitive routing decision inside a helpful-sounding message.

Finally, record the client-facing instruction. Did the client choose the partner? Did the agent provide a neutral list? Was any affiliated relationship disclosed? Was the client told they are free to shop? Was there a reason a single recommendation was appropriate? These fields make the handoff stronger because they force the team to explain the business basis before automation scales it.

The minimum workflow

The ledger should sit between the CRM signal and the outbound message.

- AI detects a service need from CRM notes, forms, calls, or transaction tasks.

- AI opens a proposed handoff record, not a direct client message.

- The ledger checks eligibility, availability, relationship flags, and client-choice requirements.

- A named human approves, edits, or blocks the handoff.

- Only then does AI draft the message, task, or introduction.

- The final message and approval evidence stay attached to the client record.

This workflow changes the role of AI. Instead of acting like a hidden recommender, AI becomes a prep assistant. It can summarize the client need, compare partner fit, draft neutral wording, surface missing data, and remind the agent to verify disclosure fields. The decision stays visible.

Fields worth tracking

A useful ledger has a small set of required fields. The exact schema can live in a CRM object, Airtable base, spreadsheet, or internal admin panel. The important part is that the fields exist before automation starts routing.

Client fields: client name, transaction stage, service need, urgency, location, preferred communication channel, client-stated constraints, and consent to be introduced.

Partner fields: provider name, category, coverage area, current availability, verification date, service-level notes, owner, recent issue flag, and approved-use categories.

Risk fields: settlement-service flag, affiliated-business flag, compensation or marketing arrangement flag, required disclosure status, client-choice status, brokerage approval status, and review owner.

Message fields: approved positioning, prohibited claims, approved disclaimer or choice language, selected next step, sent timestamp, and CRM proof link.

The key design rule is simple: no blank critical fields. If availability is unknown, AI should not invent confidence. If the relationship status is unclear, AI should route the record to a human. If the client has not approved an introduction, AI should prepare a question rather than sending the partner's contact information.

What AI is allowed to do

The handoff ledger should define clear permission levels.

Green tasks are low risk. AI can summarize the client need, pull partner history, draft internal notes, prepare a neutral list, and ask the client which category of help they want.

Yellow tasks need human approval. AI can draft an introduction, recommend an ordering of options, or prepare partner-specific context only after the ledger shows eligibility, disclosure status, and client-choice evidence.

Red tasks are blocked. AI should not promise partner availability, imply a required provider, conceal a financial relationship, make legal conclusions about referral compensation, or send a single settlement-service provider as the default when the record requires client choice or brokerage review.

This is where FTC AI enforcement themes are relevant even outside formal compliance work. The agency's AI page continues to show active enforcement around deceptive AI claims and consumer harm. A real estate team does not need to wait for a regulator to define every edge case before adopting the obvious standard: AI should not overstate certainty, hide material context, or convert an internal preference into a client-facing recommendation.

How to start this week

Pick one referral category first. Lenders, inspectors, title contacts, insurance, movers, contractors, attorneys, and home-service vendors do not all carry the same rules or risk. Start with the category where the team sends the most introductions and where mistakes create the most client pain.

Export the last 30 handoffs. For each one, identify who requested it, what the client needed, which partner was used, whether alternatives were offered, whether any relationship or compensation context existed, whether the partner was available, and whether the outcome was logged. This gives the team a baseline without debating theory.

Then create the first ledger view. Use required fields for client need, partner eligibility, availability, disclosure status, client-choice status, human owner, and approved message. Connect it to the CRM stage that triggers the handoff. Add one automation rule: AI may draft but may not send when any required field is blank or any risk flag is yellow or red.

After two weeks, review blocked records. The blockers are not a nuisance; they are the operating system. If many records are blocked because partner availability is stale, the team needs a verification cadence. If many are blocked because agents do not know which relationships require disclosure, the team needs brokerage guidance. If many are blocked because clients asked for choice but the workflow only supports one partner, the messaging system needs a neutral-list path.

The operating principle

Referral automation should make handoffs clearer, not more opaque. The best system is not the one that sends the fastest introduction. It is the one that can prove the client need, partner fit, relationship context, client choice, and approval trail before the introduction is sent.

A referral handoff ledger gives real estate teams that proof. It lets AI help with preparation and documentation while keeping judgment, disclosure, and client trust where they belong: visible, owned, and reviewable.

Sources

- NAR: Realtors Embrace AI, Digital Tools to Enhance Client Service, September 18, 2025.

- Cotality: 75% of homebuyers expect AI in process but still want human in the loop, April 16, 2026.

- CFPB: Regulation X section 1024.14, current version accessed May 5, 2026.

- CFPB: RESPA FAQs, updated October 7, 2020 and accessed May 5, 2026.

- CFPB: Pay-to-play digital comparison-shopping platform guidance, February 7, 2023.

- FTC: Artificial Intelligence topic page, accessed May 5, 2026.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile